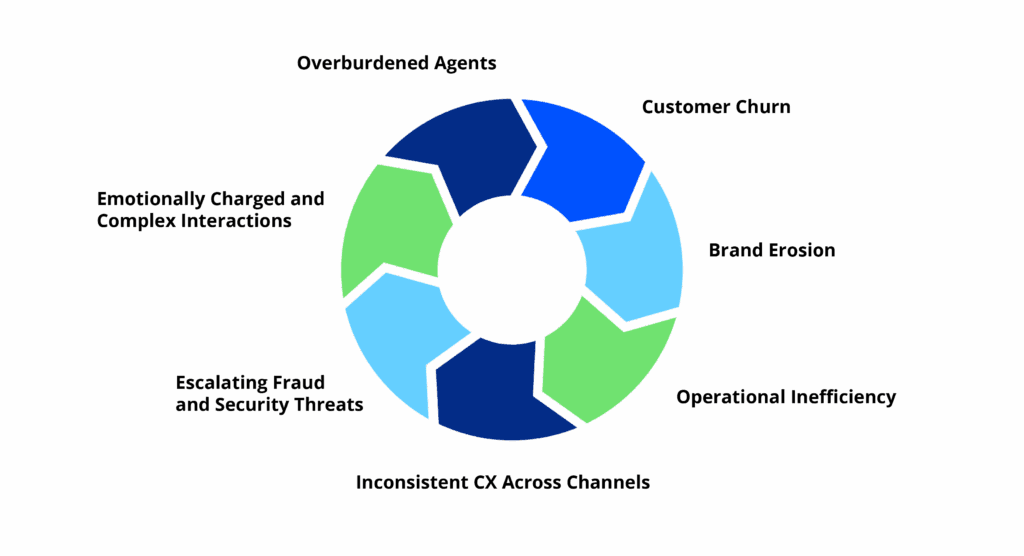

Before we look at the relationship between humans and AI, it’s important to understand the challenges faced by contact center leaders in the BFSI space. Unlike retail or travel, every customer interaction in BFSI carries regulatory weight, emotional intensity, and direct financial consequences. When a customer’s money, claim, or financial security is at stake, expectations skyrocket and the margin for error disappears. Here are the most pressing challenges shaping the future of BFSI contact centers:

Customer Churn

Consumers today judge banks and insurers as much on experience as on products. PwC found that nearly 80% of consumers say experience is as important as offerings, and human support is key to that perception. Without empathy in critical moments, customers don’t just get frustrated; they leave. And in banking, when a customer exits, they take multiple accounts, cards, and future loans with them.

Brand Erosion

Every poor bot interaction chips away at an institution’s reputation. In finance, trust is not just “nice to have”; it is the product. Bain & Company found that a 5% boost in retention can increase profits by 25–95%. Losing even a fraction of loyal customers because of a soulless bot interaction can cost millions in lost lifetime value.

Operational Inefficiency

What looks efficient on paper can backfire in practice. McKinsey reports that up to 60% of bot-handled interactions in BFSI escalate to humans because the bot fails to resolve the issue. This creates double work; customers repeat themselves, and agents start from scratch. What was meant to save costs actually bloats them.

Inconsistent CX Across Channels

Today’s customer doesn’t stick to one channel. They start with mobile, switch to chat, and escalate to a call. Yet most automation is siloed. Gartner found that 70% of customers expect companies to deliver consistent experiences across channels and when this doesn’t happen, it drives dissatisfaction and churn.

Escalating Fraud and Security Threats

Contact centers in BFSI are high-value targets for fraudsters. Between 2024 and 2025, digital fraud increased by ~21% in financial services (Veriff). Leaders must balance rigorous identity verification with smooth, low-friction customer experiences. One misstep can either compromise security or alienate legitimate customers, both of which come at a high cost.

Emotionally Charged and Complex Interactions

Conversations around denied loans, lost funds, or disputed claims are not transactional. They are personal and emotionally intense. These situations demand empathy, discretion, and human judgment, none of which bots can replicate. At a time when customers are emotionally attached to a financial brand 39% more likely to adopt new services, 32% more likely to seek advice, and are ~49% more likely to increase balances (BAI), leaders need effective resources.

Overburdened Agents

Bots often deflect the easy questions, leaving agents with only the hardest, most emotionally charged cases. Yet without AI support, agents spend 30% of their time simply searching for information across disconnected systems, says a report from Deloitte. Burnout follows, attrition rises, and customers feel the downstream impact of stressed-out staff.

The stakes are far too high to leave BFSI customers in the hands of automation alone. Money, trust, and security are on the line. While AI-powered chatbots, self-service portals, and IVR systems excel at routine queries, they often stumble when nuance, judgment, and empathy are required. That’s why the future isn’t AI versus humans; it’s AI with humans.

AI-augmented agents combine the speed and precision of automation with the empathy and contextual judgment only people can provide. Together, they deliver outcomes that consistently reflect a white glove level of service, the kind that builds lasting loyalty.

A major BFSI client was struggling to deliver cost-effective customer care. Demand outpaced their onshore team, calls went unanswered, and frustration threatened retention. UnifyCX implemented a nearshore delivery model with dedicated, security-vetted agents and layered in our AI toolkit: Study Buddy for faster onboarding and continuous learning, Agent Assist for real-time customer insights and next-best actions, 100% QA Monitoring & Coaching to score every interaction and trigger rapid feedback loops, and Voice of the Customer analytics to uncover sentiment trends and upsell opportunities.

A major BFSI client was struggling to deliver cost-effective customer care. Demand outpaced their onshore team, calls went unanswered, and frustration threatened retention. UnifyCX implemented a nearshore delivery model with dedicated, security-vetted agents and layered in our AI toolkit: Study Buddy for faster onboarding and continuous learning, Agent Assist for real-time customer insights and next-best actions, 100% QA Monitoring & Coaching to score every interaction and trigger rapid feedback loops, and Voice of the Customer analytics to uncover sentiment trends and upsell opportunities.

The results were transformative: quality scores consistently hit ~95% (exceeding the 90% goal), over 80% of calls were answered within 20 seconds, and Average Handle Time stayed on target while resolution quality improved. This combination of scale and AI not only improved CX but also boosted retention and unlocked new revenue opportunities, turning a cost center into a growth engine.